It feels like it’s been months, but it’s only been a few weeks since the world’s central banks started forcing down their key interest rates to historical lows around the world. In those places where rates weren’t reduced, the central banks have adopted vast quantitative easing plans. In some places, central banks have both reduced rates and adopted new QE.

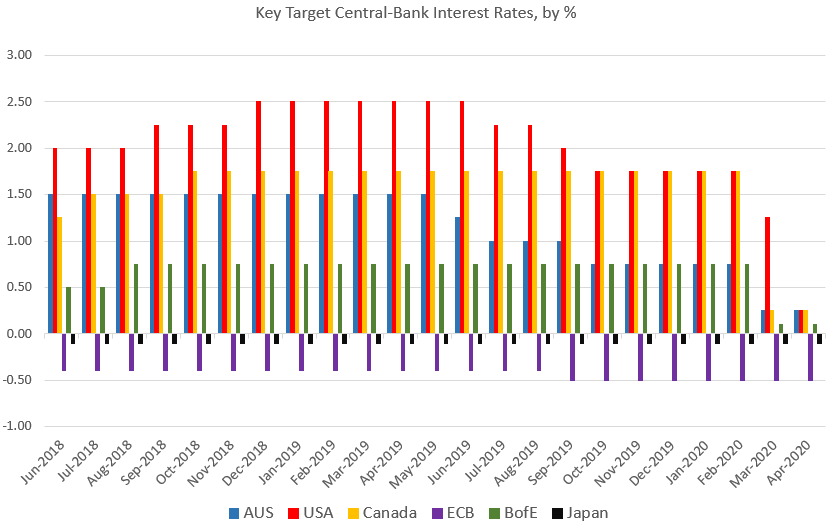

Some central banks acted earlier than others. Both the European Central Bank (ECB) and the US’s Federal Reserve knew that this already weak economy was further weakening back in late summer 2019. The Fed reduced the key rate from 2.5 to 1.75 percent from June to October. The ECB reduced its negative rate of -0.4 percent even further to –0.5 percent in September.

Rates began to collapse in March, however. The Fed met twice in March, reducing rates first to 1.25 percent, and then down to 0.25 percent shortly after that. Also in March, the Bank of Canada and the Bank of Australia reduced their key rates to 0.25 percent. The Bank of England reduced its key target rate to 0.1 percent.

The Bank of Japan announced its key rate would remain unchanged at –0.1 percent.

New Quantitative Easing

While Japan is holding its target rate steady, there will also be plenty of new QE. The Wall Street Journal reports:

The BOJ maintained its target for short-term interest rates at minus 0.1% and its target for the 10-year Japanese government bond yield at around zero….The BOJ has been purchasing exchange-traded stock funds at an annual pace of ¥6 trillion, or about $56 billion, and it said Monday it would double that target to ¥12 trillion for now. It also introduced a new program to help banks lend to companies hit by the virus and expanded purchases of commercial paper.

Meanwhile, the Bank of England isn’t even bothering to use the euphemism “quantitative easing.” The B of E is now straight up handing over new money to the Treasury to fill its massive budget shortfall:

The UK has become the first country to embrace the monetary financing of government to fund the immediate cost of fighting coronavirus, with the Bank of England agreeing to a Treasury demand to directly finance the state’s spending needs on a temporary basis. The move allows the government to bypass the bond market until the Covid-19 pandemic subsides, financing unexpected costs such as the job retention scheme where bills will fall due at the end of April. Although BoE governor Andrew Bailey opposed monetary financing earlier this week, Treasury officials felt it was best to have the insurance of the central bank willing to finance its operations in the short term.

In Europe, the ECB on March 18 announced a new €50 billion “emergency purchase programme.”

With the ECB, we might to some extent describe this as “more of the same,” since Europe appears to have have been the least inclined of the West’s big central banks to scale back its QE programs even at the height of this past decade’s (tepid) boom. Back in 2012, then ECB president Mario Draghi famously declared that the ECB would do “whatever it takes” to save the eurozone. The ECB hasn’t ever given much reason to doubt that it will at least attempt this. But this latest round is not quite more of the same, since this new round of purchases will not be constrained as the QE of the past was. Bloomberg reports:

Government bonds rallied across the euro area after the ECB released a legal document that said the issue limits, which constrained sovereign bond-buying to a third of each of its member state’s debt, “should not apply” to its new program.

Eurozone member states are now free to pile on even more debt than before. In Europe, the political stakes are very high, since Italy never really recovered from the last recession and has had a banking system teetering on the brink for years. Italy has been propped up by the ECB in a variety of ways, and with its economy now in virtual free fall, Europeans in other parts of the the eurozone (especially Germans) will have to take a big hit to their savings to keep it solvent. The political fallout may be significant.

Canada (a nation with a population and economy about the size of California’s (and with a budget of about $350 billion)), began its own new round of QE two weeks ago. In late March, the Bank of Canada announced that the “Bank will begin acquiring Government of Canada securities in the secondary market. Purchases will begin with a minimum of $5 billion per week, across the yield curve.”

As the National Post notes,

It’s a moderate start to what some analysts are predicting will be hundreds of billions of dollars in purchases of Canadian government bonds in coming months as part of the central bank’s efforts to ease strains in the financial system and keep money cheap for borrowers. The Bank of Canada hasn’t set a limit on purchases.

In Australia (where the population and economy is about the size of Texas), the Reserve Bank of Australia has announced:

“Really nothing is off the table,” RBA Governor Philip Lowe said in Sydney after giving a speech on the newly announced measures.

“We are in extraordinary times and we’re prepared to do whatever is necessary to make sure funding costs in Australia are low and the supply of credit is there for Australian businesses and households.”

The Australian approach appears to be less centered on the central bank. The Australian state has expressed plans for a wide variety of plans for fiscal stimulus and, “in a separate statement, the government said it would buy A$15 billion of residential mortgage-backed securities and other asset backed securities over the next 12 months.”

Of course, if the Australian government must turn to deficit financing for these purchases, the central bank will end up supplying the needed cash.

A World without Savings

We’re quickly finding out what a world without savings looks like. All those claims we heard from central bankers for years about how a “savings glut” was forcing down interest rates are less convincing than ever. It is increasingly clear that central banks are among the only institutions out there with an appetite for buying assets. This, of course, is because central banks can create money from nothing, while much the world is on the edge of insolvency. Those institutions that appeared to be profitable were really only making ends meet because of past bailouts and continuing low-intensity QE programs. They were “zombies.”

After decades of ultralow rates coming out of governments and central banks obsessed with maximizing consumer spending, we find ourselves with debt loads that far outstrip savings. Without central banks, there would be massive global deflation. This would hurt many financial institutions, of course, but it would also lead to a decline in stock prices, real estate, and prices for other assets that have been propped up—to the benefit of bankers, hedge fund managers, and billionaires—for decades. This would mean greater affordability for many and a badly needed restructuring of the global economy.

The only way out is to allow freedom to interest rates and to allow the financial sector to take the hit. If interest rates were allowed to reflect market demand, they would quickly increase and real savings would quickly increase as people with the means to save would have finally an incentive to put their money somewhere other than the stock market and other industries that survive primarily due to the assumption that governments and central banks will always bail them out. Resources would then begin to flow again toward assets involved directly in production of goods and services. Real production would increase, easing the supply shock.

[RELATED: “What If the Fed Did Nothing?,” by Noah Bonn]

As it is, central banks will instead focus on helping the financial sector. But the financial sector has little incentive to make loans to households and institutions in the real economy. So long as the economy is in a high-risk zone—whole central banks are simultaneously propping up demand for stocks, bonds, and a handful of other assets—it makes more sense for the financial sector to sit on the same safe assets that it has been accumulating for years. Why lend to a small business when the Fed will make sure your mortgage-backed securities are a safer alternative? So long as global trade can pave the way for more affordable goods and services, a limited escape hatch is possible. But given the current supply problems, that escape hatch may be unreachable for a long while. The pain in the meantime will be extensive for many. But don’t worry—many billionaires’ portfolios will be fine. Central banks will make sure of it.