Saturday, October 11, 2008

…Its Hour Come Round At Last… (Important Update)

**

“When Black Friday comes

I’ll stand down by the door

And catch the grey men when they

Dive from the fourteenth floor

When Black Friday comes

I’ll collect everything I’m owed

And before my friends find out

I’ll be on the road

When Black Friday falls you know it’s got to be

Don’t let it fall on me.”

A little more than a week ago, emissaries from the Power Elite fanned out on Capitol Hill to bribe, brow-beat, and threaten congressmen into passing the Economic Dictatorship Enabling Act.

The Boot: Headquarters of the Bank of International Settlements in Basel, Switzerland.

The Boot: Headquarters of the Bank of International Settlements in Basel, Switzerland.

We were told that the last argument they deployed to break down the resistance of recalcitrant representatives took the form of a terrorist’s ultimatum: Either give us what we want, or economic misery and armed violence will ensue, in the form of a global market meltdown and troops on the streets of American cities.

I suspect that the truth is even more sinister than what we were told, that the actual threat took the form of the rapist’s instructions to his victim: “It’s going to happen anyway, so you might as well stop resisting and get it over with.”

The basis for that suspicion is found in the fact that passage of the “rescue” package that would supposedly obviate a market meltdown was followed immediately by the most dramatic market plunge in history, eclipsing even the worst decline that took place during the Great Depression. So we managed to get both the creation of an economic dictatorship and a fully realized market collapse.

It is entirely likely that we will likewise see overt martial law measures put in place in the near future, as well.

If, as some very capable analysts anticipate, the short-term commercial credit system were to seize up, one immediate result would be shortages at grocery stores and gas stations. [See the Update below; this process is already underway.]

Our just-in-time commercial supply system runs on just-in-time financing, after all. And most American households, which are operated on a paycheck-to-paycheck basis, are woefully unprepared to deal with the shortages and dislocations that would result if store shelves were suddenly denuded, and gas station fuel tanks went dry.

If, as we have reason to fear, municipal and state governments start to default on their debts, then the teeming hordes of public employees may be left without their share of official plunder. We’re being advised that crime rates among the, ahem, common people tend to soar during times of severe economic hardship.

What would be the result were widespread unemployment suddenly to hit the huge and ever-growing population of tax-feeders — who are often people with an exceptionally well-developed sense of entitlement, and accustomed to a living based on coercive extraction, rather than mutually beneficial free commerce? To what extent would their hardships translate into an upsurge in (private) crime? We don’t know; we’ve never confronted this problem before.

With the cognoscenti of the G-7 and IMF now meeting in Washington, there is open discussion of a possible global “market holiday” in order to retro-fit a new rule set into the global financial markets.

The rules for the “new Bretton Woods,” according to the G-7’s latest communique — a document that manages to wed brevity and opacity in such a way as to communicate nearly nothing of value, a remarkable bureaucratic accomplishment — will be based on the recommendations of the Financial Stabilization Forum (FSF), an obscure group whose secretariat has its headquarters at the Bank of International Settlements in Basel, Switzerland.

That boot-shaped edifice was seemingly designed to reflect Orwell’s description of the totalitarian future — a “boot stamping on a human face, forever.”

The chief author of the guidelines for what Commissar for Plutocratic Redistribution Henry Paulson calls the “international regulatory response” to the global market convulsions is an all-but-unknown Italian banker by the name of Mario Draghi, Chairman of the FSF. The G-7, according to Paulson, is “committed to tackling the next steps laid out by Chairman Draghi to be done by the end of this year….”

Surely — you’re thinking — this enigmatic Mr. Draghi is the epitome of independence and sober objectivity! Surely, he is untainted by conflicts of interest that might detract from his ability to devise a wise and equitable regulatory scheme!

Surely, you jest.

Mr. Draghi’s brief but informative vita, circa 2004, proudly notes that he “joined Goldman Sachs as a partner in January 2002 and is Vice Chairman and Managing Director.”

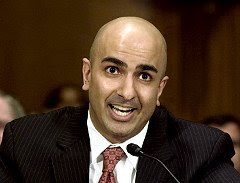

That’s the same Goldman Sachs once headed by Chief Commissar Paulson, of course. It’s the same outfit to which Paulson directed a huge portion of the $85 billion lent to AIG so that their top echelon management could continue their lives of exemplary asceticism and self-denial. It’s the same talent pool from which Paulson selected the new Sub-commissar for financial stability, 35-year-old former Goldman Sachs executive Neel Kashkari. And it’s the same entity in which Herr Paulson continues to have extensive investments, as well.

At the hub: Mario Draghi, Chairman of the Financial Stabilization Forum at the Bank of International Settlements.

At the hub: Mario Draghi, Chairman of the Financial Stabilization Forum at the Bank of International Settlements.

But what’s going on right now is not just a hugely amplified version of the same State-enabled crony capitalism that precipitated the present crisis.

Yes, the Nomenklatura is taking care of its own, and using unimaginably huge amounts of plundered wealth to do so.

But the real story here is the creation, under the pressure of an unprecedented financial crisis, of a global apparatus of wealth redistribution larger and more powerful than anything ever conceived by Lenin’s diseased brain.

As Ambrose Evans-Pritchard of the London Telegraph points out, Washington “has taken over the entire credit system … surpassing Roosevelt’s New Deal. The US has guaranteed the $3.5 trillion money market funds. It has nationalized the $5.3 trillion pillars of the mortgage market, Fannie and Freddie. The Fed is accepting any junk as collateral at its lending window. This week it went the whole hog after panic hit the $1.6 trillion market for commercial paper. It is now offering loans without any security at all.”

“The US government has become a bank,” concludes Evans-Pritchard. “Yes, this is US socialism. What is the alternative?”

The alternative, of course, would be for our economy to absorb the terrifying shocks made inevitable by decades of government-abetted fraud, and then proceed in exactly the opposite direction from the one we’re headed.

(K)neel before Goldman Sachs, peasants! Newly appointed sub-commissar for “economic stability” Neel Kashkari (left),who should not to be confused with either the evil Raza from the Summer blockbuster Iron Man (below, left), or the endearingly self-enraptured Sam the Eagle from The Muppet Show.

This would mean radical reductions in government spending — beginning with an immediate end to the wars in Iraq and Afghanistan. That one policy change alone could still conceivably save our economy.

Evans-Pritchard and other communicants in the Church of Keynes insist that the only way to deal with the global depression into which we are sinking is to emulate the behavior of FDR during the period to which history will someday refer as the “Lesser Depression.” In fact, we could do worse than to adopt some elements of the neglected 1932 Democratic Party Platform.

That document, in some ways, actually criticized the Hoover Administration from the right. It called for “a federal budget annually balanced on the basis of accurate executive estimates within revenues” (although the engine of revenue was to remain the Marxist abomination called the progressive income tax).

The Democrats called for restoration of “a sound currency,” preferably to be backed by silver; the “removal of of government from all fields of private enterprise except where necessary to develop public works and natural resources in the common interest,” thereby at once invoking a sound principle and nullifying it through proposed action.

The platform also repudiated foreign aid in principle by opposing cancellation of foreign debts to Washington, and foreswore an interventionist foreign policy by pledging to pursue “peace with all the world” and “no interference in the internal affairs of other nations….”

Granted, the platform was burdened with a generous amount of left-populist nonsense, and was entirely disregarded by FDR once he had used it to climb to power. But it attests to the fact that in 1932, amid near-universal economic ruin and inescapable despair, there was still widespread understanding of the fact that recovery would require radical reduction in the size, expense, and intrusivess of government, and eschewing foreign adventurism. FDR and his cabal, having marketed themselves to the electorate on those terms, proceeded in exactly the opposite direction, thereby exacerbating and prolonging the Depression.

The Standard Narrative of the Great Depression, as Dr. Robert Higgs of the Independent Institute points out, is based on three phases: The Great Decline of 1929-1933; the “Great Duration” until the outbreak of World War II; and the “Great Escape” as productivity and prosperity supposedly returned by way of the definitive government enterprise, war.

As Higgs reminds us, it was the end of the New Deal and the abolition of the war economy that lifted our economy out of the depression. “The year 1946, when civilian output increased by about 30 percent, was the most glorious single year in the entire history of the U.S. economy,” Higgs writes. “By 1948, real output was back on its long-run growth trend, and during the decades that followed, the economy was spared the sort of deep and long debacle that a congeries of wrongheaded government policies had caused during the 1930s.”

That blessed interval came to an end in August 1971, when Richard “We Are All Keynesians Now” Nixon de-coupled the dollar completely from the gold standard, in tacit acknowledgment that waging war in Asia while building a domestic welfare state had rendered Washington bankrupt. Thanks to the petro-dollar entente with Saudi Arabia, which preserved the dollar’s status as the world’s reserve currency, we’ve been able to avoid the consequences of national bankruptcy.

Until now.

As the song says, when Black Friday comes, “you know it’s got to be.” There has to be a Day of Reckoning. It can be deferred, but not forever. Herr Paulson and his comrades have generously arranged for the rest of us to suffer the consequences of their corruption and cupidity. After all, they can’t be distracted from the task of building a new global economic order based on the same practices and policies that have led our nation to ruin.

UPDATE — It’s Already Begun….

“The credit crisis is spilling over into the grain industry as international buyers find themselves unable to come up with payment, forcing sellers to shoulder often substantial losses,” reported Canada’s National Post last Wednesday (October 8).

“Before cargoes can be loaded at port, buyers typically must produce proof they are good for the money,” continued the Post. “But more deals are falling through as sellers decide they don’t trust the financial institution named in the buyer’s letter of credit, analysts said.”

Bill Gary, President of the Oklahoma City-based Commodity Information Systems, confirms that this developing crisis is a product of the accelerating disintegration of the banking system: “There’s all kinds of stuff stacked up on docks right now that can’t be shipped because people can’t get letters of credit…. The problem is not demand, and it’s not supply because we have plenty of supply. It’s finding anyone who can come up with the credit to buy.”

This is just one of several potential cataracts in the supply system, which depends in large measure on independent truckers who are likewise going to find it difficult to get short-term credit.

“We’ve got a nightmare in front of us and a lot of people are concerned it’s going to get a lot worse,” warns Vancouver-based grain industry analyst Anthony Temple.

“What some companies are saying is we can’t pay you until our customer pays us, so it becomes a question of who bares [sic] the financial risk and the cost,” adds Jason Myers, head of the Canadian Manufacturers and Exporters trade association. “We’re hearing about it more and more.”

The credit crunch may prove to be as devastating as a trade embargo, which wouldn’t be a problem for the United States if we still had a self-sufficient market economy. It’s worth noting at this point that the United States — once the breadbasket of the known universe — recently became a net importer of food.

On sale now!

Dum spiro, pugno!

Content retrieved from: http://freedominourtime.blogspot.com/2008/10/its-hour-come-round-at-last.html.