Tuesday, October 7, 2008

What Rough Beast… (EXTREMELY Important Second Update, 10/8)

The October Revolution of 2008 will prove to be at least as consequential as the one that occurred in Russia in 1917.

Beginning immediately after 9-11, George W. Bush and the cabal he represents began the controlled implosion of the hollowed-out shell of our once-sturdy republic. Last week the final phase of that demolition project got underway.

By using monetary inflation as a sapping device, the FED is knocking down the few federalist pillars that, at least in theory, separated the various layers of government. It is also preparing to nationalize key segments of the commercial economy. All of this is being done through the FED’s New Deal era “emergency powers” to extend “credit” to any entity it chooses, whether governmental, commercial, or “public-private partnership.”

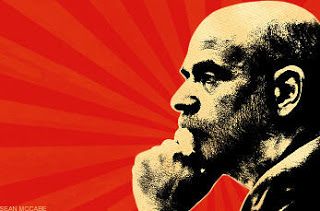

The “Lenin” of America’s October Revolution: Chief Fed Commissar Ben Bernanke

The “Lenin” of America’s October Revolution: Chief Fed Commissar Ben BernankeThe revolution of 1913-1933, which inflicted the Federal Reserve, income tax, and the New Deal apparatus upon the United States, left us with a system Mussolini described as a “corporate state,” more commonly known as Fascism.

Admittedly, the American version was milder than most, at least domestically. The Revolution of 2008 is consolidating the elements of that system into a monolithic, unitary State of the sort Lenin and his heirs would applaud, were they not busy suffering for eternity in hell.

The creation of the Federal Reserve in 1913 was a partial enactment of the fifth plank of the Communist Manifesto, which called for creation of “a national bank with State capital”; last week, with the creation of a de facto economic dictatorship under the Secretary of the Treasury, Congress implemented the other key element of that plank, “centralization of credit in the hands of the state.”

Approval of the new economic dictatorship was the irreducible purpose of the so-called Economic Stabilization Act, which — true to the measure’s pedigree of grandly named government interventions — has summarily failed to stabilize the economy.

The $700 billion disbursed by the bill was a trifle, in light of the magnitude of the debt flood to be “bailed out” and the ability of the FED to create what it’s pleased to call “money” in any amount it chooses. But that relatively trivial amount was enough to create a constituency for the bill not only on Wall Street, but also in statehouses, city halls, and wherever else the Horseleach’s Daughters convene.

“Yes, we can!” Hey, guess what? Before Stalin became one of history’s most prolific mass-murderers, he was a “community organizer,” too! Here he helps mobilize support for the little exercise in idealism called the Bolshevik Revolution.

With both the corporatist and political elements of the parasite class enlisted to support the revolution, all that remained was the neutralize the productive class — the common people, who found ourselves on the bad end of what the reliably perceptive Chris Floyd calls “one of the largest single redistributions of wealth since the Bolsheviks seized power in Russia in 1917.”

Unanimity is, almost without exception, a bad thing in politics. The near-unanimity of the electorate in rejecting the Wall Street “bailout” measure is one of those incalculably precious exceptions. In the teeth of this near-unanimity, Congress — led by the Senate, supposedly the more deliberative chamber — took the rejected bill, an austere 3-page Enabling Act for the economic dictatorship, plumped it up with several hundred pages of bureaucratic boilerplate and undisguised pork, and passed it four days later.

Bribing a Congressman is generally about as challenging as seducing Catherine the Great. Getting the institution to surrender its institutional control over the public purse was a bit more difficult. Some Congressmen — well, at least one, perhaps two or three others — recalled their duty to their constituents, as well as their constitutional mandate to control the public purse, and held fast. Many others opposed the Enabling Act/Plutocrat Bailout because of simple terror over the prospect of immediate unemployment.

But in this case, bribery was coupled with undisguised official terrorism — the use or threatened use of violence to achieve a radical change in the political system.

As Brad Sherman, a Democratic Congressman from California, testified in a remarkable address on the House Floor — an address the likes of which will soon be punishable as sedition — that representatives of the Regime candidly informed recalcitrant congressmen that refusal to pass the Enabling Act would result in nothing less than “martial law in America.”

Subsequently, many people, including Rep. Sherman himself, sought to minimize the significance of those threats, describing them as manipulative hyperbole rather than a credible threat. This would be something on the order of a frantic lobbyist exclaiming that failure of the bailout would lead to real “Wrath of God-type stuff” — the stock market collapsing, permanent constipation of the credit markets, shortages, troops on the streets, human sacrifice, dogs and cats living together, mass hysteria.

The jolly jokesters representing the White House and the Bankster Elite were just exaggerating for effect, you see.

The problem with that explanation, of course, is that the Bush Regime is actively preparing for martial law. So is the German government. So is the British government. Most likely, so are other governments throughout the Euro-Zone, and everywhere else central banks are still coupled to the rapidly disintegrating dollar.

The problem with that explanation, of course, is that the Bush Regime is actively preparing for martial law. So is the German government. So is the British government. Most likely, so are other governments throughout the Euro-Zone, and everywhere else central banks are still coupled to the rapidly disintegrating dollar.

There is no way we can honestly construe the comments reported by Rep. Sherman as anything other than a legitimate, credible threat to accomplish, through a coup de main, what Congress was being ordered to do: Surrender its power over the purse to an executive branch department that is an appendage of Wall Street.

This time, the mere threat of direct military action was sufficient. Next time, we may see putsch come to shove. But the real problem is this: The willingness of congressional majorities to be complicit in this betrayal most likely means there won’t be a “next time” — another occasion in which public outrage, coupled with the threat of quick voter retaliation, prompts Congress to act in the public good.

Go ahead and vote this November, if you can find national candidates unsullied by this consummate betrayal. But a higher priority should be to anticipate, and prepare for, the severe dislocations that are about to occur in our everyday life as the collapse accelerates and deepens.

As credit lines grow more constricted, shortages of gasoline and grocery items become more likely. Fill your pantry with non-perishable foods that don’t require much preparation. Secure an adequate supply of drinking water. Network with informed family and like-minded friends and, if possible, keep an inventory of emergency supplies. If you can build a small fellowship of that kind, it’s a good idea to have a designated meeting place to gather and pool resources in the event of a severe emergency. Toward that end it’s also a good idea to keep your gas tank topped off, or nearly so, if this is economically feasible.

Don’t confide in the idea that you will always have access to cash via an ATM, even if your deposits (like mine) aren’t within a parsec of the new $250,000 FDIC limit. Owners of 401(k) accounts are learning in the worst possible way about the evanescence of virtual “wealth” as some two trillion dollars of that hypothetical commodity disappear into the ether.

For that reason, it’s wise to keep a supply of tangible money. Yes, of course, that means silver — particularly pre-1964 “junk” coins — and gold. It also means keeping a supply of ready cash on hand in the form of the depreciating but still useable FRNs.* In the event of a “bank holiday,” you won’t be permitted to withdraw cash, and it’s likely that debit cards wouldn’t work. So keeping sufficient cash on hand for a month’s expenses is a wise precaution.

It is my fondest hope that the advice offered in the foregoing paragraphs will prove to be the product of unwarranted alarmism.

I experienced exactly the same sentiment last March when I first suggested that “panic” of that variety was a perfectly rational course of action; I had the same desperate eagerness to be wrong last March 7, when — citing analyses offered by much better minds than my own — I predicted on Dr. Stan Montieth’s radio program that the long-anticipated financial collapse would begin in late September or early October.

Maybe I’m entirely wrong now. May God grant that it be so. But don’t count on it.

Update: Happy (Bank) Holidays…?

His Imperial Ineptness is going to convene an emergency international finance summit, most likely in Washington. With Iceland and Pakistan on the brink of national bankruptcy, and the contagion raging out of control, we may see an international bank holiday very soon.

Get liquid, right now.

And, as poster Dixie Dog reminds us (and I stupidly neglected to), this is an exceptionally good time to pray.

Second Update: “Regime Change” Through Inflation

When Thomas Jefferson famously warned Treasury Secretary Albert Gallatin that “banking institutions are more dangerous to our liberties than standing armies,” this is the kind of thing he almost certainly had in mind:

“Having tried without success to unlock frozen credit markets, the Treasury Department is considering taking ownership stakes in many United States banks to restore confidence in the financial system.”

The plan being discussed in the Olympian realm of the Power Elite is reportedly similar to the ongoing nationalization of Great Britain’s banking system. At the same time, notes the New York Times, “investors are clamoring for the Fed to lower interest rates to nearly zero. Some are also calling for governments worldwide to provide another round of economic stimulus through expensive public works projects.”

Predictability offers some comfort, I suppose, in these turbid and troubling times, which is why there’s something winsome and reassuring in the knowledge that people will still seek “solutions” from Keynes’s syllabus of economic errors. Perhaps the “public works” in question would be, as Keynes suggested, hiring one body of men to dig holes, and another to fill them. Or our rulers might combine the expense and futility of that exercise with massive death, terror, and destruction and simply arrange a ripping good war, the public works project for which government has displayed a singular aptitude.

Indeed, as the Times points out in words that chill any perceptive person to the marrow, we’ve already reached the phase at which those who presume to manage our destinies are talking about the “moral equivalent” of war:

“Fed officials increasingly talk about the challenge they face with a phrase that President Bush used in another context: `regime change.’ This regime change refers to a change in the economic environment so radical that, at least for a while, economic policy makers will need to suspend what are usually sacred principles: minimal interference in free markets, gradualism and predictability.”

Reverse-engineering the FED’s intention from that report, it’s clear that we’re in for maximal interference in, or abolition of, free markets, accomplished suddenly by people who exercise power capriciously.

In other words — an October Revolution brought to us by the Banksters without their Bolshevik middle-men.

And by the way….

Imitation is the sincerest form of … Birchism, I guess. Then again, if those folks hadn’t done this, maybe they’d occasionally be on top of relatively significant developments, such as the terminal unwinding of the global financial system….

___

*FRNs = Federal Reserve Notes, the intrinsically worthless pieces of tastelessly decorated rag paper the Regime insists we refer to as “money.”

It’s more timely than ever, and it’s on sale now.

It’s more timely than ever, and it’s on sale now.

Dum spiro, pugno!

Content retrieved from: http://freedominourtime.blogspot.com/2008/10/what-rough-beast.html.