Wednesday, February 20, 2008

Our Collapsing Kleptocracy (UPDATED)

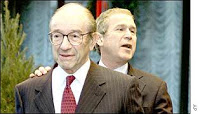

The frontman looks for cover: Bush cowers behind former Fed Commissar Alan Greenspan, architect of the debt bubble that is devouring the world economy.

TODAY correspondent Ann Curry: Some Americans believe that they feel they’re carrying the burden because of this economy.

George W. Bush: Yeah, well…

Curry: They say we’re suffering because of this.

Bush: I don’t agree with that.

Curry: You don’t agree with that? It has nothing do with the economy, the war, the spending on the war?

Bush: I don’t think so. I think actually the spending in the war might help with jobs.

Curry: Oh, yeah?

Bush: Yeah, because we’re buying equipment, and people are working. I think this economy is down because we built too many houses and the economy is adjusting. —

TODAY Show, February 18

Occasionally the Mass Murderer-in-Chief will make a candid comment that serves as a core sample of his personality. Beneath the superficial affability that disguises his inbred sense of unearned privilege, below the dense-pack arrogance, hidden away under multiple layers of ignorance and corruption, at the center of his being, Bush is a creature of the kleptocratic State, in its crudest and most destructive form.

It’s not just that Bush has completely internalized a dimwit’s version of Keynesianism. He also appears genuinely to believe that war –heedless wholesale destruction — is more profitable than constructive private enterprise.

“Y’see” — I can imagine him saying in his practiced mock-drawl, his shoulders hunched over in that oddly simian way of his, a self-satisfied smirk creeping across that face that could have been designed by Matt Groening – “these idiots in the private sector jus’ went out and built a whole buncha houses nobody could afford, an’ now we gotta big mess. Don’t know why the fools went and overbuilt the housing market. Here’s the cool thing, though: You can’t overbuild the military. Heck, if we build too many bombs, or tanks, or missiles, we can always find some use for ‘em, and if we can’t, I’m sure the Israelis or the Saudis or someone can take ‘em off our hands – even if we have to pay them to.”

While Bush is well-known for his significant contributions to the practice of military Keynesianism, he has played no small role in expanding the practice of the domestic version as well – including the same vastly overbuilt housing and mortgage market.

The unwinding of the sub-prime mortgage market is what triggered the ongoing – and ever-escalating – global financial crisis. Bush (who probably thinks the term “sub-prime” refers to a steak that costs less than a C-note) probably doesn’t remember that he was directly involved in abetting the sub-prime disaster. Yes, the Fed created the mortgage mess as a matter of deliberate policy. But Bush did his considerable best to help things along.

“Low interest rates have encouraged a housing boom here in America–and that’s good, that’s good,” Bush exulted at an October 2003 forum on Hispanic-American affairs in California, years before he “discovered” that a housing boom is a Bad Thing. In the same speech, he urged that banks make more “zero down payment loans available to first-time buyers[,] whose mortgages are guaranteed by the Federal Housing Administration….”

If you want more of something – in this case, risky mortgage loans to dubiously qualified borrowers – subsidize it. And the subsidies that aided the housing bubble didn’t come only through the FHA, of course. Fannie, Freddie, and Ginnie all got into the act, as well, creating a world-historic debt bubble that is now rapidly collapsing. This wasn’t done out of an altruistic desire to help every American own a home, but because the politically connected investor class realized unfathomably huge profits in generating that debt and finding perversely creative ways to repackage it.

In a sane world, that would be a noose, rather than a medal — and both of them would be on the scaffold. (I’m kidding. Sort of.)

As James Howard Kunstler* points out, our present financial system is nothing more than a “daisy-chain of liabilities” – beginning with the “dollar” itself, an instrument of debt posing as a form of currency.

Kunstler chose an unfortunate name for his must-read blog (caveat lector), and his assumptions regarding “Peak Oil” are disputable. He is entirely correct, however, in predicting an impending economic depression he calls the “Long Emergency,” and his analysis of the financial system strikes me as sound.

Bogus deity, real money: An ancient Greek silver coin bearing an image of the goddess Artemis.

Where once every national currency was backed by “reserves” of something considered valuable – generally gold – “reserves” came to be “denoted in just currencies themselves, or certificates that represented the existence of currencies held elsewhere, or pixels on a screen representing the movement of alleged piles of currency from one place to another, or the intention to move a notional pile of currency to a theoretical destination, and then that became an algorithm purporting to represent the future arrival of a notional pile of money at theoretical destination-to-be-named-later, and so on…. And after a while, the nature of money became so detached from anything real, so abstract, that its very existence became hypothetical. Even this `worked’ for a while, in terms of the managers of this money being able to `cream’ substantial amounts of this hypothetical money off the top of their notional operations and translate that hypothetical cream into Tribeca lofts, Gulfstream jets, and other real luxuries.”

“The rest of the economic food chain” – meaning serfs like thee and me – “got stripped of remaining asset value … until they had nothing left to trade with except debt, in one form or another, and this phase of the game turned out to have a short lifetime when the only debts remaining to be monetized were the contracts on houses occupied by people with no hope of ever meeting their obligations – and then the whole sorry racket started to go up in vapor.”

At present, the banks – with the quiet help of Helicopter Ben’s counterfeiting agency – “are pretending to have money and desperately cadging loans from all comers to keep appearances up, but the loans can’t come in fast enough.” At some point, somewhere in this purportedly wealthy country, news will leak out that an inconspicuous bank is about to fail. This will trigger a bank run, and the contagion will spread far and fast.

That’s what happened last September at England’s Northern Rock bank, that country’s fifth-largest mortgage lender. Northern Rock quietly applied to the Bank of England for emergency aid to prevent a bank run. Instead, it precipitated one.

In the course of a single weekend, before the government guaranteed Northern Rock’s deposits and police turned away panicky customers, the bank lost some $4 billion as customers emptied their accounts. As the Economist magazine notes, this was England’s first bank run since 1866. Just a few days ago, the British government announced – after failing to arrange a subsidized take-over by Richard Branson’s Virgin Group — that it was nationalizing Northern Rock.

Consider this: Richard Branson is willing to risk life, limb, and fortune in his effort to pioneer commercial spaceflight, but he wants nothing to do with the banking business unless the taxpayers provide him with parachute.

Right now, as noted above, American banks are doing exactly the same thing that triggered the run on Northern Rock: They’re on life support to the central bank, hoping to forestall depositor panic. But, once again, at some point, a significant bank failure will happen, a run will materialize and metastasize – and, as Kunstler writes, “that would be the magic moment that the USA discovered it was no longer a rich nation.”

Northern Rock may yet prove to be the pebble that starts a global financial avalanche. Or that catastrophe may begin somewhere on this side of the Atlantic. But it is coming, and probably sooner than most people think.

The last Depression we endured took place in a country with enviable natural resources, a large and growing industrial capacity, and blessed with a population familiar with discipline, thrift, and the deferral of gratification. The next depression, Kunstler predicts, “will play out against the background of a society that has pissed away its oil endowment, bulldozed its factories, arbitraged its productive labor, destroyed both family farms and the commercial infrastructure of main street, and trained its population to become overfed diabetic TV zombie `consumers’ of other peoples’ productivity, paid for by `money’ they haven’t earned.”

To the extent this description of the hoi polloi is accurate, the behavior described reflects the priorities of the ruling oligarchy, in which – perhaps to an extent unprecedented in our history – fortunes are made through the vulgar redistribution of wealth by the State. And in this respect, George W. Bush is a perfect exemplar of his class.

In his infuriating and informative new book Free Lunch: How the Wealthiest Americans Enrich Themselves at Government Expense (And Stick You with the Bill), David Cay Johnston recounts the old and sadly neglected story of how Bush the Younger became wealthy. Like Kunstler, Johnston is mistaken in some important ways, but he does an admirable job exposing the machinations of our ruling oligarchy, of whom Bush the Lesser is a suitable specimen.

During the reign of Bush the Elder, Duhbya was wealthy, but not extravagantly so. Unlike Joseph in Egypt, under whose hand every venture prospered, Bush the Younger had a knack for running businesses into the ground. His was the touch of Tantalus, rather than Midas.

Bush did know how to manage one asset only a handful of Americans enjoy: His family political connections, many of which we reinforced by his inherited membership in Yale’s Skull & Bones secret society. (Depending on whom you ask, Skull & Bones is either a satanic coven or an oddly packaged Good Old Boy network; my view is that it is a little of both.)

“Yeah, we may look like the founders of the Paul Anka Fan Club — but trust us, we’re evil“: George “Poppy” Bush (immediate left of the Grandfather Clock) and fellow Bonesmen.

Unlike his father or his grandfather, Bush the Younger didn’t take his Bonesman duties all that seriously. As an initiate, he was given the new name “Temporary” as a placeholder until he thought of a more appropriate sobriquet, and he never bothered to change the default. So to this day, Bush the Younger remains “Temporary” to his Bonesman brethren.

In the early 1990s, several Bonesmen were among the investors Bush turned to when he conceived the idea of buying the Texas Rangers. The underperforming team wasn’t a bargain at any price, but Bush believed that the Rangers could quickly become profitable if a new stadium could be built for them. In fact, the investors quickly devised a plan to build a 200-acre “entertainment zone” surrounding the new stadium, including hotels and restaurants.

Bush and his cronies could easily afford to buy the Rangers; they could even afford to build a stadium. But getting the land to build the “entertainment zone” would be a little more difficult, since many of those who owned the property weren’t interested in selling.

Ah, I see that at least some of you know where this story is headed….

Rather than paying what the owners would have been willing to take for their land, Bush and his buddies “simply had the city of Arlington seize the land they needed and more, using government’s power of eminent domain,” recalls Johnson.

The new stadium was built by a municipal “Sports Authority” (represented in court by Ray Hutchison, husband of Texas Republican Senator Kay Bailey Hutchison). The Authority was funded through a half-cent increase in sales tax approved in a quick and dirty referendum held after Bush threatened to move the Rangers to another city – a now-familiar extortion tactic by owners of professional sports teams seeking municipal subsidies. It also administered an interest-free rent-to-own arrangement for the team’s new owners, with every payment – and all maintenance expenses – applied to the purchase price of the stadium.

“The investors Bush assembled paid $86 million for the Rangers,” summarizes Johnson. “They sold nine years later for $250 million. The $164 million profit was $38.5 million less than the [total] subsidy” provided through the Authority. As a result, “Every dollar that Bush and the other investors pocketed when they sold the team came from the taxpayers…. Bush and his investors made no economic profit from the market when they sold the team. The only money they received came from the increased sales taxes that flowed into the stadium deal” – and that deal was made possible by the theft and extortion carried out through eminent domain.

In many ways, Bush’s Arlington Scam prefigured the much larger and infinitely more murderous criminal enterprise called the Iraq War. In Texas, Bush used the power of eminent domain to seize property to enrich himself and his buddies; in Mesopotamia, he arranged a military occupation of an energy-rich nation for more or less the same purpose.

In both cases, the taxpayers were plundered for the benefit of Bush and his fellow kleptocrats, although in the case of Iraq the price is paid through the relentless debasement of the currency, and the resulting theft of our earnings and savings. Oh, yes, the costs also include the death, dismemberment, or derangement of tens of thousands of Americans sent to colonize Iraq.

But from where Bush and his comrades sit the war is a sweet deal for the economy, and it’s churlish of the rest of us to cavil over the costs of such a profitable enterprise. After all, Bush explained with an idiot child’s impression of regal generosity in the above-referenced TODAY show interview, “we’re just about to kick out 157 billion dollars to our taxpayers” in the form of tax rebates, a lagniappe that will do little more than trigger a brief and inconsequential spasm in a dying consumer economy.

The most useful thing any of us can do with that rebate is to use it – along with whatever liquid funds we can spare – to invest in some combination of the three Noble Metals: gold, silver, and lead.

UPDATE: The Contagion Spreads….

Germany’s state-owned KfW banking group, which invested billions in the US sub-prime mortgage market, is “on the verge of bankruptcy, with its supposed[ly] wonderful investments worth little more than the paper [they were] printed on,” reports Der Spiegel. And other state-owned banks are beginning to totter:

“The state of North Rhine-Westphalia has injected 1 billion [pounds] into WestLB, another state-owned bank, as well as providing the ailing bank with another 3 billion [pounds] in loan guarantees. The situation is even worse in Saxony, where the state has issued 2.73 billion [pounds] in guarantees to Sachsen LB, that state’s Landesbank, as Germany’s state-backed regional banks are known. The other state-owned banks are providing another 14 billion [pounds] in guarantees. Hamburg-based HSH Nordbank urgently needs 1 billion [pounds] in fresh capital, while Bayern LB announced Tuesday that the bank’s chief executive, Werner Schmidt, will be stepping down as of March 1 as a result of the crisis.

“The situation for Germany’s public banks has become so dramatic that it threatens to topple what has been one of the key pillars of the country’s banking system. The state-owned banks are supposed to bail each other out when necessary, but the problem is that many are in trouble themselves and hardly in a position to help their peers. And things could get even worse.”

That’s Will Grigg’s First Iron Law of Reality (c): Things can always get worse. Where the international banking system is concerned, they will get radically worse in a hurry.

(Thanks to Lew Rockwell for drawing attention to the Der Spiegel story.)

*In the original version, I mistakenly referred to James Howard Kunstler as “William” Kunstler. That’s a pretty major “whoops,” one I regret as earnestly as I appreciate a reader’s gentle correction thereof.

Point of Personal Privilege…

Please forgive the lengthy hiatus between essays. During the past two days I did something uncommon — I took the equivalent of a brief vacation. (My last genuine vacation was in August 2001, and my former employers managed to bisect that one by sending me to New York in the middle of it.) This was dictated by simple exhaustion.

Korrin has been in the hospital since early October, and even with the considerable and heroically generous help of my friends and family it’s been difficult to maintain a reasonable work schedule while being a temporary single parent to five young children. I sure appreciate your patience, and your prayers.

Owing to problems with my local ISP, this post is uncommonly light on graphics and links. When those problems clear up, I’ll probably revisit today’s edition and upgrade it considerably.

Don’t forget: My new book, Liberty in Eclipse, is available at The Right Source.

Don’t forget: My new book, Liberty in Eclipse, is available at The Right Source.

Dum spiro, pugno!

Content retrieved from: http://freedominourtime.blogspot.com/2008/02/our-collapsing-kleptocracy.html.