Monday, September 15, 2008

The Denouement (Updated)

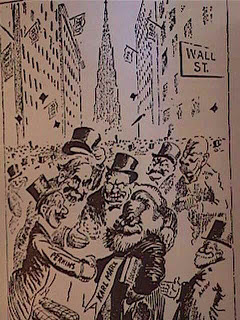

Hail comrades well met: In this famous 1911 editorial cartoon, Karl Marx is rapturously greeted on Wall Street and taken to the bosom of Carnegie and Rockefeller. This tidily sums up the relationship between Wall Street corporate socialists and the non-housebroken Marxist revolutionaries who are their distant kin.

Denouement (n) — The unraveling of a plot; a catastrophe….

From Webster’s Unabridged Dictionary (1913)

There is something supernally appropriate to the fact that, in order to find the most suitable definition for just right word to describe the ongoing crisis of the financial system, we have to refer to a dictionary published in 1913.

We are now into the second year of the unraveling of the world financial system. It could be described as the Great Denouement (or final act) of a plot that began in 1913, when Congress created the Federal Reserve System, aka the Focus of Evil in the Modern World. So far the effects of the unraveling have had minimal impact on the larger economy.

This is about to change.

Last Friday, there were five globe-bestriding Wall Street investment banks. Today there are three. Lehman Brothers, a 158-year-old financial colossus, is headed for bankruptcy and oblivion. Merrill Lynch, which was following the same trajectory, was bought by Bank of America.

Tellingly, the markets greeted that acquisition by selling off Bank of America shares, despite CEO Ken Lewis’s happy prattle about the “synergies” supposedly catalyzed by this buy-out. Likwise, the bank’s credit rating took a hit following the transaction. This is exactly the opposite of what we would expect to see when one business demonstrates its vitality by purchasing another. In this case, however, it is well understood that BofA wasn’t gaining assets, but rather taking on an infection.

Over the same cluttered weekend, American International Group, which insures (among other things) corporate bonds, played the mendicant at the Fed’s discount window, pleading for $40 billion in tide-us-over money while it tries to liquidate assets in order to raise cash. [For more about AIG, see the update below.]

While we’re accustomed to weekly bank failures and periodic federal bailouts, the converging meltdowns of three pillars of Wall Street in a single weekend indicates that the crisis is accelerating and deepening in ways that our financial overlords hadn’t anticipated. The fact that Lehman was permitted to fail demonstrates that the overlords are now beginning to conduct triage among themselves — a spectacle that might offer the some brief amusement for the hoi polloi until the survivors within the Power Elite turn their undivided attention on the rest of us.

It’s likely that some distant day, when the history of the Greater Depression is written, the collapse of Lehman Brothers will be seen as a climacteric for the Fed-centric financial system — indeed, for Washington’s entire apparatus of imperial power, in which that investment house played a conspicuous role.

Mapping the catastrophe (click to enlarge).

Mapping the catastrophe (click to enlarge).

During the mid-1800s, Lehman provided much of the initial financing for the railroad combine, one of the first serious ventures in American corporatism. That combine, a public-private partnership — a prototype for what Mussolini later called Fascism — thrust Abraham the Abhorrent into the White House, where he presided over a war of national consolidation and pioneered the concept of a dictatorial war presidency.

Following the destruction of the pre-1861 Union of free states and creating a unitary Corporate State, the combine engaged the services of the United States military to drive the Plains Indians from lands pledged to them by treaty, but also coveted by the combine to build its federally subsidized transcontinental railroad. This relationship was a distant but recognizable ancestor of the modern military-industrial complex.

Lehman was part of the cartel that pushed for creation of the Fed. Its roster of corporate leaders bristles with insider credentials; senior management officials held prestigious posts on the Federal Reserve Board, in the World Economic Forum, and in the Council on Foreign Relations. And yet the firm is now bound for bankruptcy, a casualty of the Fed’s housing/mortgage/refinancing bubble. Pulling the plug on Lehman Brothers may be equivalent to the sharp tug on a dangling thread that causes the entire tapestry to unwind.

Unlike the bailout of Bear Stearns earlier this year, no takers could be found when Henry Paulson and Ben Bernanke tried to find a buyer for Lehman Brothers. Would-be buyers were repelled by the aroma of Lehman’s assets, which was quite similar to that emitted by an artificial butte constructed out of not-so-gently-used disposable diapers.

When it became clear that no rescue could be arranged for Lehman, the bankster mafia did the next best thing: It opened the markets — just a crack — to let a handful of favored investors minimize their losses. The manipulation was as undisguised as the contempt the banksters feel for the torpid and indifferent public that is being plundered on behalf of the financial elite.

Lehman CEO Richard Fuld, known as “The Gorrilla” because of his penchant for alpha male-style posturing, was able to keep the firm intact during the last big scare, the Asian debt crisis of a decade ago.

Learning exactly the wrong lessons as a result of that corporate near-death-through-debt experience, Fuld threw his company into issuing and securitizing mortgage loans. During the last two years, long after rational people had sought protection from the bursting of the housing/mortgage bubble, Lehman was the nation’s largest underwriter of mortgage bonds.

Last March, by which time Fuld must have been fully aware of his bank’s afflictions, he accepted a $22 million performance bonus, based on a supposed net profit of 5 percent in 2007. Surely there are people just as qualified as Fuld to lead a company to immediate ruin who would have done so for less than one percent of what Lehman paid Fuld. The bank’s Chapter 11 filing lists $613 billion in debts. This is not only the largest private bankruptcy in history, it must also rank as the largest act of non-governmental accounting fraud on record.

A few weeks later — April 15, to be exact — Fuld inscribed his name indelibly in the Big Book of Hubristic Quotations when he told shareholders that “the worst is behind us.”

As recently as August, Fuld could have taken advantage of buy-out or buy-in offers that would have rescued his firm. But the CEO, looking at his company’s worth through the distorting lens of bubble-vision, insisted that the offers “didn’t reflect the value he saw in the bank,” according to the New York Times. So he dithered and dissimulated until it was much too late, perhaps in the misplaced confidence that his comrades in the financial elite would seal a deal with a taxpayer guarantee. Rather than giving him that cushion, however, his fellow elitists pulled the chair out from beneath him.

Given the Fed’s new role as “lender of last resort,” why did it permit Lehman to fail? It may be simply a matter of bad timing: Had Lehman’s terminal crisis occurred two months ago, the Fed and Treasury might have been willing to arrange another taxpayer-insured bailout. But right now the overlords have their hands full managing the nationalization of Fannie and Freddie, which may require trillions of dollars yet to be created.

Even Helicopter Ben must appreciate the point that the foreign creditors who continue to fund this racket are eventually going to stop taking dollar-shaped IOUs. That’s when the real fun will begin.

The Bailout Resumes….

AIG, valued at $1 trillion at the beginning of the trading day, “lost 70% of its value in just three hours,” reports the New York Daily News. Its stock recovered about half its losses by mid-afternoon. Meanwhile, the Governor of New York announced that he was altering state regulations — apparently by executive decree — to permit AIG “to borrow against its subsidiary assets.”

Ten of the largest American banks have announced a plan to pool $70 billion “in a collaborative effort to prevent any of them [from] running out of funds in an emergency.” Each has thrown in $7 billion, and any can borrow up to $23 billion.

That’s not a “pool”; it hardly qualifies as a puddle. And it will be gone before the end of the week.

So, in all probably, will Washington Mutual, which was dangling from a cliff, clinging to an exposed tree root at the end of last week. Lehman’s demise will almost certainly send WaMu careening into the abyss.

And there are at least 1,000 more banks headed over the edge, as well….

Gratuitous extra update —

Headline: “Doctors Remove Benign Lesion from Bush’s Forehead.”

Oh, swell — they removed the only part of him that wasn’t malignant.

On sale now!

Dum spiro, pugno!

Content retrieved from: http://freedominourtime.blogspot.com/2008/09/denouement_15.html.