")

The Bureau of Labor Statistic (BLS) released new jobs data on Friday. According to the report, seasonally adjusted total nonfarm jobs rose 339,000 jobs in May, well above forecasts. The unemployment rate rose slightly from 3.4 percent to 3.7 percent (month over month).

Headlines in the mainstream media declared the headline employment data to be evidence of very strong job growth and economic success. According to Politico, the latest jobs numbers are evidence of a “remarkable resilience of President Joe Biden’s economy” and NPR declared the job market to be “sizzling hot.”

Yet, May appears to be yet another month in which it seems nearly every economic indicator except the payroll jobs data points to an economic slowdown. The Philadelphia Fed’s manufacturing index is in recession territory. The Empire State Manufacturing Survey is, too. The Leading Indicators index keeps looking worse. The yield curve points to recession. Even Federal Reserve staffers, who generally take an implausibly rosy view of the economy, predict recession in 2023. Individual bankruptcy filings were up 23 percent in May. Temp jobs were down, year-over-year, which often indicates approaching recession.

So how do we square all this with yet another jobs report that claims to tell us that the job market is the best it’s been in decades?

Well, a lot of the jobs data isn’t actually very good. The headlines have focused on the so-called Establishment Survey which is a survey of employers and shows only the number of positions, not the number of employed persons. The Household survey, on the other hand, surveys people.

The Household survey over the past two years has not shown nearly as much job growth as the Establishment Survey.

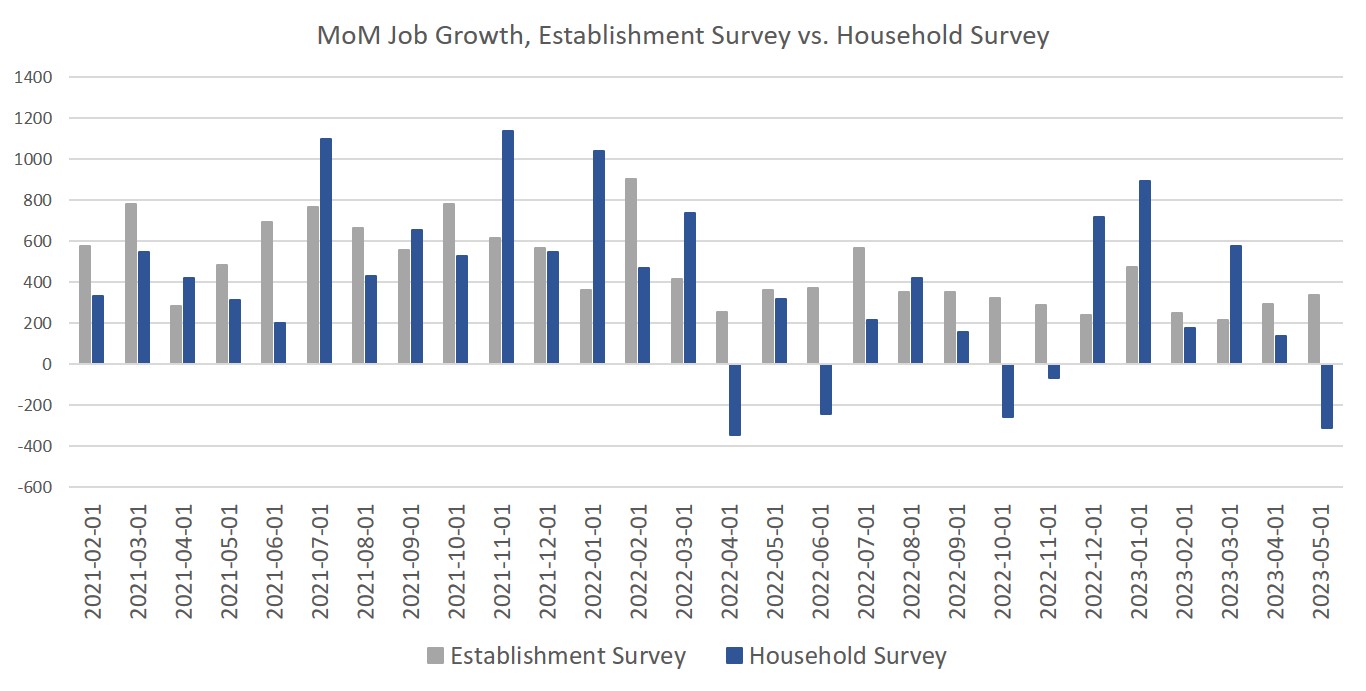

Specifically, we find that since 2022, the Establishment Survey and the Household Survey have ceased to follow a similar trend, with a sizable gap forming between the two surveys. In fact, over the past two years, the two surveys show a gap of 2.2 million:

Moreover, in May, while the Establishment Survey showed a gain of 339,000 jobs month-over-month, the Household Survey showed a loss of 310,000 employed persons. That’s a gap of more than 600,000. Looking at month-to-month changes, we can also see how the two surveys have diverged since April 2022.

Part of this growing gap may be due to the fact that the number of responses to the Establishment survey has dropped off in recent years, suggesting that the survey is waning in its reliability as an indicator of the overall economy. The Household Survey, meanwhile, has not seen as large a drop off in responses.

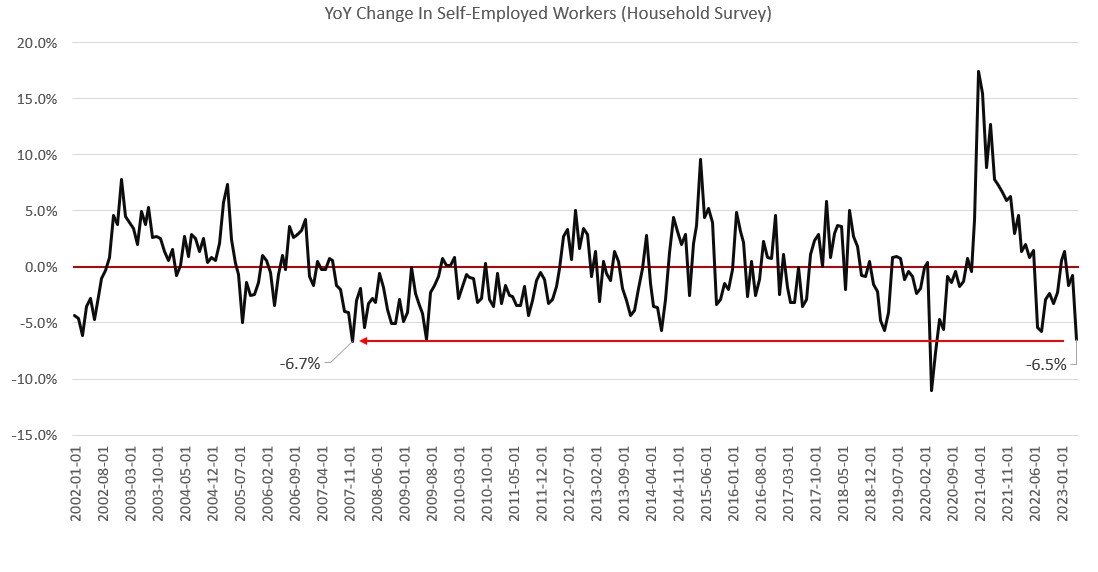

Another factor is the fact that the Establishment Survey does not track self-employed workers, and self-employment has been a significant factor in employment trends over the past three years. Self-employment collapsed in April 2020, but surged by April 2021 to historic highs. It is unknown, of course, how many of these workers were actually replacing lost income from covid-related job losses in this period. By 2023, however, self-employment had collapsed again, and year-over-year self-employment growth dropped by 6.5 percent in May. Excluding the covid lockdown period, that’s the largest year-over-year percentage drop since December 2007, when the Great Recession officially began.

We might also note that overall, the total number of payroll jobs, as shown in the Establishment Survey, is now up by 3.7 million jobs since the previous peak in March 2020 peak. The Household survey, on the other hand, shows total employed persons up by only 1.9 million persons over the same period. That’s a gap of 1.7 million.

The fact that the two different employment reports tell two different stories has led some economists to wonder about the media’s rosy jobs narrative. As reported by Yahoo Finance last week, economist Ian Shepherdson noted:

“This is the strangest employment report for some time… [R]ight now the data suggest that economic growth is stronger than is indicated by most other monthly data. The downward trend in job growth since the summer of 2021 now appears to have flattened-off, though that could change with revisions.”

And economist Paul Ashworth pointed out:

“The bigger-than-expected 339,000 increase in non-farm payroll employment in May will dominate the headlines, but the employment report was not all positive — with a big drop in the household survey measure of employment driving the unemployment rate up to a seven-month high of 3.7% and average weekly hours worked edging down to a three-year low.”

We might also note that the year-over-year gain in average hourly earnings in May (according to the Household Survey) fell to a 25-month low. If the Cleveland Fed’s “Nowcast” is right about inflation for May, then May will have been another month of falling real wages.

Part of the confusion and contradictory date no doubt arises from the fact that “jobs” are not at all homogeneous and employment trends can differ greatly across different industries and regions. This is the natural outcome of fact that monetary inflation is not at all neutral as it enters the economy—as the Austrian School has long pointed out. The current trend of rapidly decelerating monetary growth will have sizably different effects across the economy. The Establishment Survey is especially inept at capturing these trends in real time.

This article was originally featured at the Ludwig von Mises Institute and is republished with permission.